Proof of Expected Utility Property:

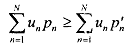

Suppose that the rational preference relation  on the space of lotteries L satisfies the continuity and independence axioms. Then admits a utility representation of the expected utility form. That is, we can assign a number u, to each outcome n = 1.. . ,N in such a manner that for any two lotteries L =

on the space of lotteries L satisfies the continuity and independence axioms. Then admits a utility representation of the expected utility form. That is, we can assign a number u, to each outcome n = 1.. . ,N in such a manner that for any two lotteries L =  , we have LL' if and only if

, we have LL' if and only if

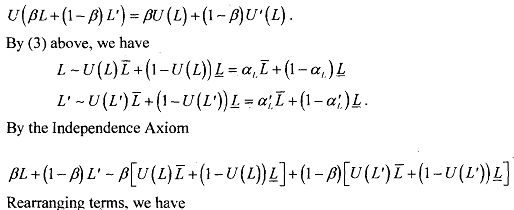

Proof: (Taken rnoslly from Aulor, 2004) Assume that there are best and worst lotteries in L, and L

1) If  (due to the indegendence axiom)

(due to the indegendence axiom)

2)

3) For any L ∈ L, there is a unique aL such that  . (due to continuity axiom)

. (due to continuity axiom)

4) The function U: L -> R that assigns u (L) = a, for all L ∈ L represents the preference relation . From (3) above for any two lotteries we have

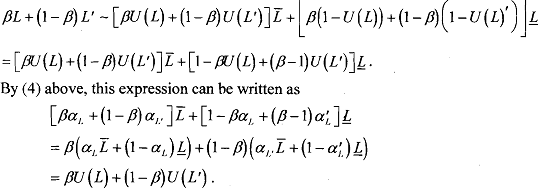

5) The utility function U(.) that assigns U(L) = a, for all L G L is linear and therefore has the expected utility form. We want to show that for any L, L' E L, and ~[0,1], we have

So, we have established that a utility function satisfying the continuity and the Independence Axiom, has the expected utility property:

In brief, we can say that, a person who has vNM expected utility preferences over lotteries will act as if she is maximising expected utility - a weighted average of utilities of each state, weighted by their probabilities. To use this model, we need a utility function that bundles into an ordinal utility ranking. Note that such functions are defined up to an affine (i-e., positive linear) transformation. This means they are required to have more structure (i.e., are more restrictive) than standard consumer utility functions, which are only defined up to a monotone transformation