Negative Externalities and Inefficiency:

As externalities are not reflected in market prices, they can be a source of economic inefficiency. Private consumption or production activities may generate costs, which are not "internalized" and not paid for by consumers or producers. As a result costs are imposed on society, which in question tends to be over-extended.

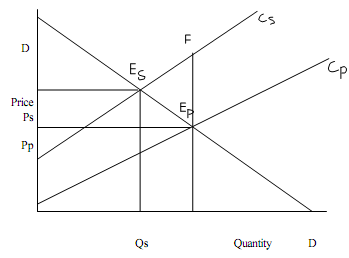

This is shown in the following diagram. External costs leads to the problem of dealing with social "bads" such as pollution and environmental damage. Let us take an example of a steel plant dumping waste in a river. The marginal private cost schedule is lower than the marginal social cost schedule by the amount of external cost due to water pollution. This is represented by the distance between both private and social cost supply curves. It is also assumed that there are no external benefits, which means social benefit = individual benefit.

In the fig:

Cs= Social Cost

Cp=Private cost

Qs=Quantity Supplied if Social Cost is taken into account

Pp=Price if only Private Cost is taken into account

Qp=Quantity Supplied if only Private Cost is taken into account

Ps=Price of Social Cost

Es= Ideal equilibrium reflecting social cost

Ep= Actual equilibrium in private market (taking account of only private cost)

DD=Marginal benefit (given by demand curve)

When external cost is considered, then production should be increased only as long as marginal social benefit (MSB) exceeds marginal social cost (MSC). If the private cost of producing steel is considered individually then the equilibrium will be at Pp and Qp, instead of the more efficient price Ps and quantity Qs. It will result in inefficiency of a free market since the production of quantity Qp indicates that marginal social benefit (Ep Qp ) is less than the marginal societal cost (FQp). Therefore the society as a whole will be better off if the production of goods between Qs and Qp is stopped. The problem still persists as the people continue buying and consuming steel.

Thus, negative externalities encourage too many firms to remain in the industry as perfectly competitive firms produce according to market incentives.