Short Run Equilibrium of the Perfectly Competitive Firm:

A firm is said to be in equilibrium at the output level where there is no incentive to alter output or supply decision e.g. at the profit - maximizing output level.

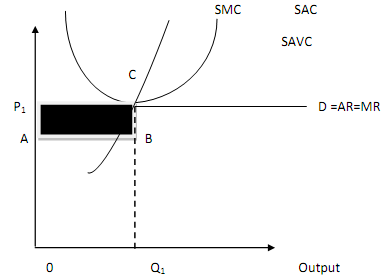

The general rule for profit-maximization is that the firm will achieve the maximum profit at the output level where marginal cost (MC) = (MR). Since in the case of perfectly competitive firm, price and marginal revenue are equal, the profit-maximizing rule can be redefined as the point (i.e. output level) where MC = MR=P. It is also necessary that at that output level, MC is rising and the firm is incurring the least cost per unit i.e. short-run average total cost (SAC) of output.

Figure: The short-run Profit-maximizing position for a Perfectly Competitive Firm

As shown in Figure , the firm maximizes its profit by producing output Q1 where MC = MR

=P. The firm's total point represented by shaded rectangle P1ABC is obtained as total revenue (rectangle P1OQ1C) less total cost (rectangle AOQ1B). Hence, the perfectly competitive firm is making positive economic profit, otherwise referred to as abnormal profit or supernormal profit in the short-run.