Error Variance Varies Directly with an Independent Variable:

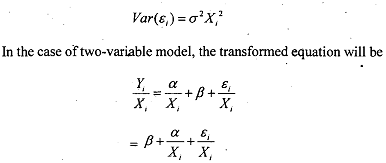

The most commonly used assumption is that σ2 is associated with a variable. If the variance of the ithobservation is proportional to the square of the explanatory variable, then deflation by this variable results in a model exhibiting homoscedasticity. Suppose the variance of the iIh observation is proportional to the square of the explanatory variable, X. Thus

Hence, the variance of the disturbance term is now constant, and we can proceed to apply OLS to the transformed equation (8.12), by regressing  . In our original regression model a is the intercept and β is the slope parameter. In the transformed regression model, however, Q is the intercept and a is the slope. Therefore, to get back the original model we need to multiply the estimated transformed model by X. Notice that by applying OLS method to (8.12) we obtain estimators which are BLUE.

. In our original regression model a is the intercept and β is the slope parameter. In the transformed regression model, however, Q is the intercept and a is the slope. Therefore, to get back the original model we need to multiply the estimated transformed model by X. Notice that by applying OLS method to (8.12) we obtain estimators which are BLUE.