Consistent estimates of variances:

With heteroscedasticity, the biased and inconsistent estimates of the variances of the OLS parameter estimates causes statistical inferences to be invalid. White (1980) has suggested a method for obtaining consistent estimates Of variance and covariance of OLS estimates which provides valid statistical tests for large samples. The heteroscedasticity-consistent estimator (HCE) is based on the principle of maximum likelihood.

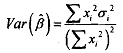

In the two-variable regression model

generates a biased estimate of thevariance of P. An unbiased estimator is

The heteroscedasticity-consistent estimator uses equation as its basis, replacing the unknown σ2 with the squares of the residuals ε. With HCE estimation, the R2 for the regression will be the same, but all estimates of standard errors and related statistics will change because they are now consistent estimates. While the use of the HCE estimator does generate consistent variance estimates, it does not provide the most efficient parameter estimates. For efficient estimation, one of the weighted least squares estimatioh procedures must be used.