Measurement Errors in both X and Y:

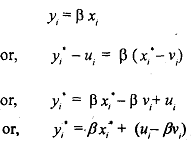

Now let us assume that both X and Y have errors of measurement. The true model is as before

Since X and Y have errors of measurement, we observe x* and y* instead of xi and yi, such that A, .

where ui and vi present the errors in the values ofyl and x, respectively. We make the following assumptions about the error terms:

(i) There is no correlation between the error term and corresponding variable, i.e.,

(i) There is no correlation between error of one variable and measurement of the other variable, i.e,,

i) There is no correlation between errors in measurement of both the variables, i.e.,

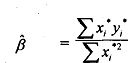

On the basis of the above assumptions, our estimated regression equation will be

Equation (9.8) shows that if we model y* as a function of x* the transformed disturbance contains measurement error in β. We then write the OLS estimaton β' as

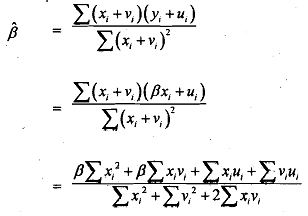

By substiuing the values of x* and y* in terms of x and y we find that

From above we observe that E(β) ≠ β.

Thus, β' will not be a consistent estimator of β. The presence of measurement error of the type in question will lead to an underestimate of the true regressiortpararneter if ordinary least squares are used.