Measurement Error in X:

We have taken the true regression model deviation form to be

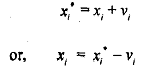

Now let us assume that explanatory variable x, is measured with error and the observed value becomes x,' such that

where  We have assumed earlier that the measurement error in x is normally distributed with zero mean, it has no serial correlation, and it is uncorrelated with E, . However, we can no longer assume that the composite error term w, is independent of the explanatory variable xi* .

We have assumed earlier that the measurement error in x is normally distributed with zero mean, it has no serial correlation, and it is uncorrelated with E, . However, we can no longer assume that the composite error term w, is independent of the explanatory variable xi* .

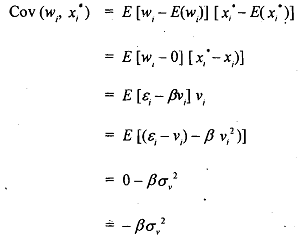

The composite error term w, has mean zero as  Thus, the explanatory variable and the error term are correlated, which violates the cpcial assumption of the classical linear regression model that the explanatory variable is uncorrelated with the stochastic disturbance term. If this assumption is violated, then OLS estimates are not only biased but also inconsistent; they remain biased asymptotically, Let us now show this.

Thus, the explanatory variable and the error term are correlated, which violates the cpcial assumption of the classical linear regression model that the explanatory variable is uncorrelated with the stochastic disturbance term. If this assumption is violated, then OLS estimates are not only biased but also inconsistent; they remain biased asymptotically, Let us now show this.

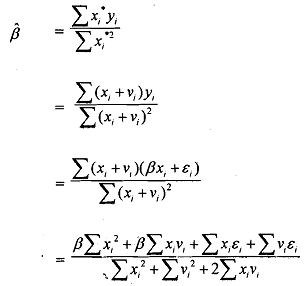

Instead of being able to estimate true relationship (9.1), we are forced to replace xi by xi*. Now the OLS estimator is

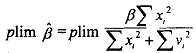

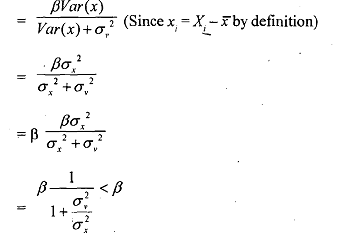

From above we find that β is a biased estimate as E(β) ≠ β. Let us see the asymptotic properties of β. Since vi and qi are stochastic and are uncorrelated with each other as well as with x,, we can say that

Thus, β' is biased even for an infinite sample and β' is an inconsistent estimator of β.