Production:

- Firms should choose how much of each to produce.

- The alternative quantities can be illustrated by using product transformation curves.

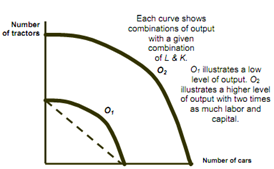

Product Transformation Curve

* Observations

- Product transformation curves are sloped negatively

- Constant returns are there in this example

- As the production transformation curve is concave is joint production desirable?

- There is no direct relationship between economies of scope and economies of scale.

- May experience diseconomies of scale and economies of scope.

- May have the economies of scale and don't have economies of scope.

* The degree of economies of scope measures savings in cost and can be given as:

- C(Q1) is cost of producing Q1

- C(Q2) is cost of producing Q2

- C(Q1Q2) is joint cost of producing both products

* Interpretation:

- If SC > 0 -- Economies of scope

- If SC < 0 -- Diseconomies of scope

* Issues

- Truckload versus less than truck load

- Direct versus indirect routing

- Length of haul