Partial Input Elasticity of Output:

This is a short-run concept which deals with the variability of only one factor keeping the others constant. There are three kinds of returns:

i) Increasing returns: when the AP of a factor rises and MP > AP

ii) Constant returns: when AP is constant and MP = AP

iii) Diminishing returns: when AP is falling MP < AP

The concept of returns to a factor can also be expressed in terms of the "partial input elasticity of output".

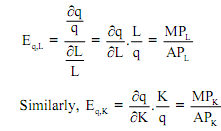

Partial input elasticity of output is also called elasticity of output with respect to a factor. It is the percentage change in output quantity for one per cent change in the quantity of a factor when all other factors remain constant.

Elasticity of q with respect to L is given by,

let us now related this to return to scale

Besides the above mentioned three returns, there can be another type known as the 'non-proportional returns to a variable factor'. Under it, initially, there is increasing returns to a factor up to a certain level beyond which there is diminishing returns.