Costs: If raw materials, machines and other things required for production could be made available freely then the study of the theory of the production and indeed, the study of economics would be useless! However, a firm has to incur costs of all kinds which demand serious attention.

• Cost Function : A cost function expresses the relation between total cost and the cost minimizing level of output. Mathematically, C = C(y) where y is the optimal output level.

• Short Run: In the short run there are 2 kinds of costs - fixed costs and variable costs. Fixed costs are the costs of the fixed factors and do not change with the changes in the level of output produced. Variable costs, which are the cost of the variable factors, change with the change in the production level.

C(y) = TC = TFC + TVC, where TC is total cost, TFC is total fixed cost and TVC is total variable cost.

If K and L are the fixed and variable factors respectively, whose prices are r and w then

TC = wL + rK.

Since L depends on the output produced,

TC = wL(y) + F where F is a constant.

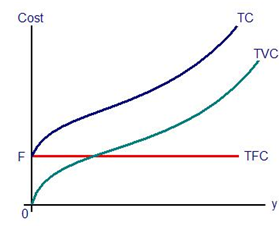

In the above graph note the following features:

i. When y = 0, TFC = F, TVC = 0, TC = F.

ii. The vertical distance between TC and TVC remains constant and is equal to F.

iii. As y rises, TVC increases and so does TC.