Consumer Behavior

The description of how consumers allot their resources (income) to the purchase of various goods and services to get maximum in their well being.

There are three steps included in the study of consumer behavior.

1) We will learn consumer preferences.

To explain how and why people select one good to the other.

2) Then we will move to budget constraints.

People have restricted incomes.

3) Then we will combine together consumer preferences and budget constraints to know about consumer choices.

What combination of goods will consumers purchase to maximize or enhance their satisfaction?

Consumer Preferences

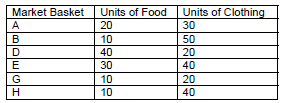

Market Baskets

A market basket is a group of one or more commodities.

One market basket can be preferred over the other market basket consisting a diverse combination of goods.

Three Basic Assumptions

1) Preferences are complete.

2) Preferences are transitive.

3) Consumers always select more of any good to less.