Choosing Output in Long Run

* In long run, a firm can change all its inputs, including size of the plant.

* We are taking free entry and free exit.

* Accounting Profit and Economic Profit

- Accounting profit (π) = R - wL

- Economic profit (π) = R - wL - rK

- wL = labor cost

- rk = opportunity cost of capital

* Long Run Competitive Equilibrium

- Zero-Profit

- If R > wL + rk, the economic profits are positive

- If R = wL + rk, zero economic profits, but firms is earning normal rate of return; showing that the industry is competitive

- If R < wl + rk, consider going out of the business

- Entry and Exit

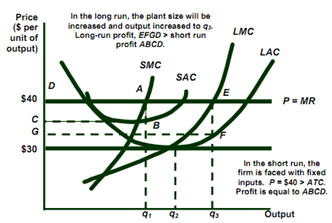

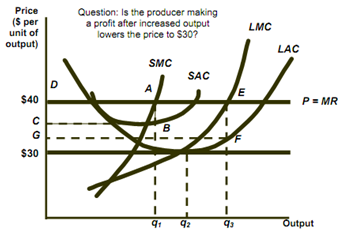

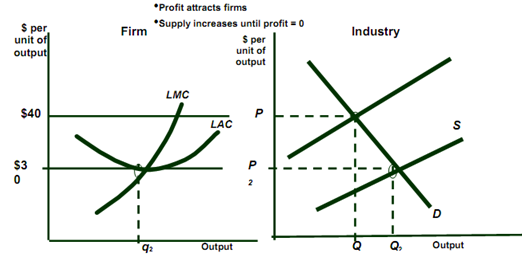

• The long run response to short run profits is to increase profits and output.

- Profits will attract the other producers.

- More producers increase the supply of industry that lowers market price.

Long Run Competitive Equilibrium

* Long Run Competitive Equilibrium

1) MC = MR

2) P = LAC

- No incentive to enter or leave

- Profit = 0

3) Equilibrium Market Price

* Questions

1) Explain market adjustment when P < LAC and firms are having identical costs.

2) Explain market adjustment when firms are having different costs.

3) What is opportunity cost of land?