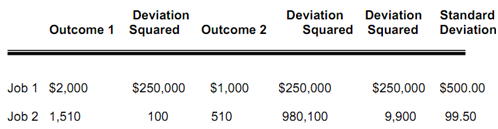

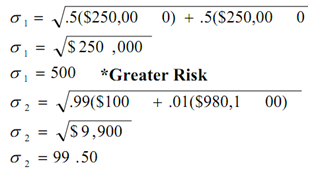

Calculating Variance (σ)

The standard deviations of the 2 jobs are:

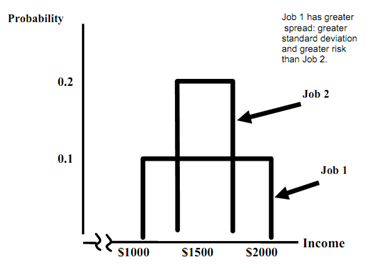

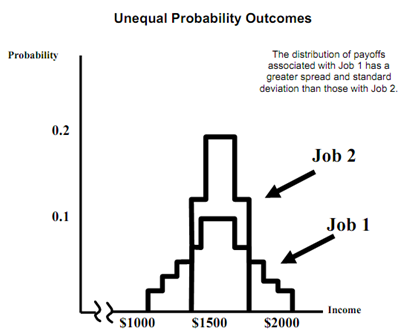

The standard deviation is used when there are several outcomes instead of only two.

* An Example

- Job 1 is a job in which income varies from $1000 to $2000 in increments of $100 which are all equally likely.

- Job 2 is a job in which income varies from $1300 to $1700 in increments of $100

that, are all equally likely.

* Outcome Probabilities of Two Jobs

- Job 1: bigger spread and standard deviation

- The peaked distribution: extreme payoffs are much less probable

*? Decision Making

- A risk avoider would select Job 2: same expected income as Job 1 with less risk.

- Assume that we add $100 to each payoff in Job 1 which makes expected payoff = $1600.

The standard deviation is square root of deviation squared.

*? Decision making

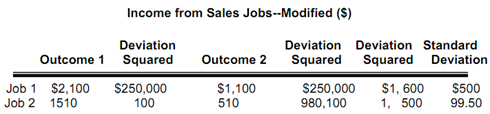

- Job 1: the expected income is $1,600 and a standard deviation of $500.

- Job 2: the expected income of $1,500 and a standard deviation of $99.50

- Which job?

- Greater value or less risk?

*? Example

- Suppose a city wants to deter people from wrong parking.

- The alternatives ......

* Assumptions:

1) Wrong parking saves a person $5 in terms of time spent searching for a parking space.

2) The driver is risk neutral.

3) Cost of apprehension is zero.

* A fine of $5.01 would deter the driver from double parking.

- Benefit of wrong parking ($5) is less than the cost ($5.01) equals the average benefit which is less than 0.

* Increasing fine can reduce the cost of enforcement:

- A $50 fine with a .1 probability of being caught results in the expected penalty of $5.

- A $500 fine with a .01 probability of being caught results in the expected penalty of $5.

* The more risk reluctant drivers are, lower the fine is required to be in order to be effective.