Reference no: EM131019295

Second Midterm

Use the following information to answer the next question.

Suppose that a firm uses wood in the production of wooden chairs. The details about the technology are displayed in the table below.

|

Inputs

|

Wood (pieces)

|

4

|

8

|

12

|

|

Outputs

|

Chairs

|

1

|

2

|

4

|

1. According to the information given above, in the range of production between 1 and 2 chairs, the technology displays

a. Increasing returns to scale.

b. Decreasing returns to scale.

c. Constant returns to scale.

d. Economies of scale.

2. Average total cost equals average variable cost when:

a. The marginal cost is zero.

b. Marginal cost equals average variable cost.

c. Marginal cost equals average total cost.

d. Fixed costs are zero.

3. Which of the following must be always true as the quantity of output increases?

a. Marginal cost must rise.

b. Average total cost must rise.

c. Average variable cost must rise.

d. Average fixed cost must fall.

Use the following information to answer the next three questions.

In the perfectly competitive market for cellular telephones, the demand is given by the following equation: Pd = 80 - 3*Qd, and the marginal cost curve for each identical firm is given by: MC = Qs + 4, and the long-run equilibrium price in the market is $8.

4. What quantity of output will each firm produce in the long-run equilibrium?

a. 2 units

b. 4 units

c. 6 units

d. 8 units

5. How many firms will be in the market in the long-run equilibrium?

a. 1 firm

b. 2 firms

c. 4 firms

d. 6 firms

6. Suppose that in the short-run the price in the market is $6. Which of the following is true?

a. Firms will make zero economic profit in the short-run.

b. There will be exit of firms in the long-run.

c. Firms will make negative profits in the long-run.

d. There will be entry of firms in the short-run.

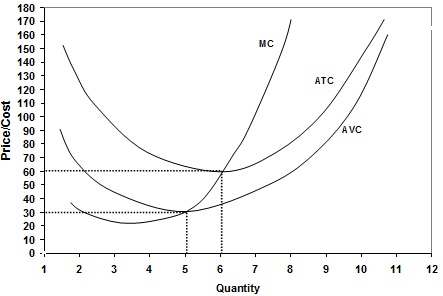

Use the following graph to answer the next two questions.

7. Suppose the market for concrete is perfectly competitive, and the price in the market is currently $50. Which of the following best characterizes the state of the market?

a. There are positive profits in the short-run.

b. There will be entry of firms in the short-run.

c. Firms will shut down in the short-run.

d. Firms will produce in the short-run and exit in the long-run.

8. Suppose demand for concrete is perfectly inelastic at a quantity of 300 units. How many firms will exist in the long-run if the market for concrete is perfectly competitive?

a. 6

b. 50

c. 60

d. 120

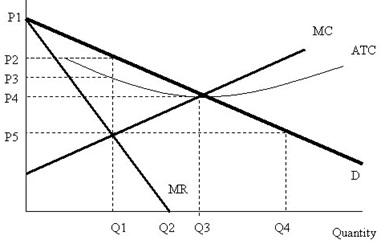

Use the graph below to answer the next two questions

9. What is the profit-maximizing price for this monopolist?

a. P2

b. P3

c. P4

d. P5

10. What is the value of consumers' surplus generated by this monopolist?

a. 0.5*(P1-P3)*Q1

b. 0.5*(P2*Q1)

c. 0.5*(P1-P2)*Q1

d. 0.5*(P1-P4)*Q3

11. Which of the following statements is True?

a. A natural monopoly typically sets marginal revenue equal to average cost.

b. A natural monopoly displays a large cost advantage due to economies of scale.

c. A good example of a natural monopoly is McDonalds.

d. A natural monopoly exhibits price-taking behavior.

Use the following table to answer the next two questions.

This is the accounting data for the production and cost of San Francisco's Muni (Bus) System.

|

Q

|

VC

|

MC

|

AVC

|

FC

|

TC

|

AFC

|

ATC

|

|

0

|

|

|

|

A

|

300

|

|

|

|

1

|

|

|

B

|

|

|

|

375

|

|

2

|

C

|

55

|

|

|

|

|

D

|

Note: Q: quantity, VC: Variable Cost, MC: Marginal Cost, AVC: Average variable cost, FC: Fixed Cost, TC: Total Cost, AFC: Average fixed cost, ATC: Average total cost

12. What are the values of A and B, respectively?

a. 300, 375

b. 200, 75

c. 200, 375

d. 300, 75

13. What are the values of C and D?

a. 110, 355

b. 110, 215

c. 130, 215

d. 130, 355

14. Which of the following statements is TRUE?

a. Firms choose a quantity where marginal revenue equals marginal cost in a perfectly competitive market but not in a monopoly.

b. Firms have the ability to set the market price in a monopoly but not in a perfectly competitive market.

c. There are a large number of buyers in a perfectly competitive market but not in a monopoly.

d. Firms maximize economic profits in a perfectly competitive market but not in a monopoly.

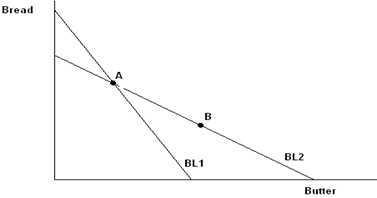

Use the following graph to answer the next question.

15. On the graph above point A represents the consumer's optimal consumption bundle when facing BL1 and point B is the consumer's optimal consumption bundle when facing BL2. (Note that point A is on both BL1 and BL2). We can say that:

a. Point A is preferred to point B

b. Point B is preferred to point A

c. Point A and point B are equally preferred

d. We can not say anything about preferences between points A and B.

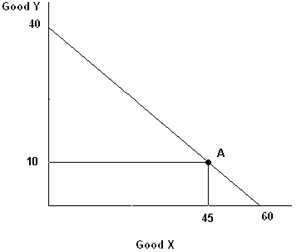

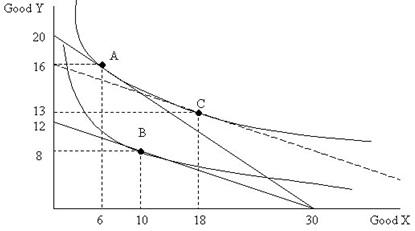

Use the following graph to answer the next three questions.

16. If Jane has six dollars then the price of good Y is ____ and the price of good X is ____.

a. $0.15, $0.20

b. $0.20, $0.15

c. $0.20, $0.10

d. $0.15, $0.10

17. If point A was Jane's optimal bundle what would Jane's marginal rate of substitution be at that point?

a. 2/9

b. 2/3

c. 3/2

d. 9/2

18. Now suppose that point A is no longer the optimal consumption bundle and that at point A Jane's marginal rate of substitution is 1. Jane would be sure to increase her utility by:

a. Moving a small amount along her budget line to the right, increasing consumption of good X.

b. Moving a small amount along her budget line to the left, decreasing consumption of good X.

c. Consuming 60 units of good X and 0 units of good Y.

d. Consuming 40 units of good Y and 0 units of good X.

Use the following graph to answer the next two questions. Note: this graph is NOT DRAWN TO SCALE.

19. From this graph we can see that good X is _______ and good Y is _________.

a. normal, normal

b. normal, inferior

c. inferior, normal

d. inferior, inferior

20. Assuming this individual has $60, derive the equation for the demand curve of good Y, where P is the price of good Y and Y is the quantity demanded. (You need to assume that the demand is linear!)

a. P = 7 - 1/4 Y

b. P = 4.5 - 1/8 Y

c. P = 1 - 1/4 Y

d. P = 7 - 4Y

21. In order to know the optimal consumption choice for the consumer, we need to know the

a. consumer's preferences.

b. consumer's budget line.

c. market supply curve.

d. both (a) and (b).

Use the following table to answer the next two questions.

| Year |

CPI |

Nominal wage |

Real wage |

| 1980 |

200 |

$10,000 |

|

| 1990 |

300 |

|

$7,000 |

| 2000 |

400 |

$30,000 |

|

22. What will be the CPI measure in year 2000 if we alter the base year to 1980.

a. 100

b. 200

c. 300

d. 400

23. According to the table above, which of the following statements is True?

a. The Real wage in 1980 is $20,000.

b. The Nominal wage in 1990 is approximately $2,333.

c. The consumer's purchasing power is increasing over time.

d. Inflation from 1980 to 1990 is the same as inflation from 1990 to 2000.

24. Suppose the band Spinal Tap needs guitars and amplifiers to perform a show this weekend. They would like to have as many guitars as they can, but they need exactly one amplifier for every two guitars. Guitars cost $30 to rent and amplifiers cost $15. If they have $150 to spend, how many guitars will they rent?

a. 2

b. 3

c. 4

d. 5

Use the following information to answer the next two questions.

|

Price

|

Quantity

|

Total Cost

|

|

300

|

0

|

300

|

|

250

|

3

|

740

|

|

150

|

5

|

980

|

|

100

|

9

|

2480

|

|

50

|

12

|

3000

|

|

0

|

15

|

5800

|

25. If fixed cost is decreased by $100 for the firm shown in the table above, the marginal cost of one additional unit when the firm is initially producing a quantity of 3 will

a. Stay the same.

b. Decrease.

c. Increase.

d. Be uncertain since there is not enough information given to answer this question.

26. At which output level could the firm make a positive economic profit?

a. 3

b. 5

c. 9

d. 12

27. What is the main difference between accounting profits and economic profits?

a. Accounting profits take into account sunk costs whereas economic profits do not.

b. Accounting profits are not as rigorously calculated as economic profits.

c. Accounting profits take into account only explicit costs whereas economic profits consider both explicit and implicit costs.

d. Economic profits are usually larger than accounting profits.

28. The long-run equilibrium price under perfect competition is determined by ____.

a. the minimum of the variable cost curve.

b. the minimum of the marginal cost curve.

c. the minimum of the average total cost curve.

d. the minimum of the average fixed cost curve.

29. Which of the following is NOT a characteristic of perfect competition?

a. In the long run, firms earn zero economic profits.

b. The individual firm has the ability to affect the market price.

c. There is free entry and exit of firms.

d. There are a large number of firms.

30. Price _________ marginal cost in a perfectly competitive market, and price _________ marginal cost in a monopoly.

a. is less than, equals

b. is more than, equals

c. equals, is less than

d. equals, is more than

Use the following information to answer the next two questions.

A monopolist has the following cost functions: TC=60Q + 240 and MC=60. The market demand for this good is given by P = 120 - Q.

31. How many units of the good does the monopolist produce?

a. 30 units

b. 35 units

c. 20 units

d. 40 units

32. What is the maximum profit generated by the monopolist?

a. $635

b. $660

c. $700

d. $560

33. A natural monopoly is producing an output level of 10,000 units per day. If the monopoly is broken up into 10 equal sized firms, then average total cost for each of the 10 firms

a. Will exceed the monopolist's average total cost.

b. Will equal the monopolist's average total cost.

c. Will be below the monopolist's average total cost.

d. May be higher or lower than the monopolist's average total cost.