Reference no: EM132657910

Question 1: Let Z be a standard normal random variable, and let g be a differentiable function with derivative g'. Note: Assume that g(x) ∈ o(exp(x2)) with E(|g'(x)|) < ∞. where g(x) ∈ o(h(x)) means limx→∞ g(x)/h(x)= 0.

a. Show that E(g'(Z)) = E(Z g(Z)).

b. Show that E(Zn+1) = nE(Zn-1)

c. Find E(Z4).

Question 2:. Suppose Xt i.i.d~N(μ,σ2) with μ > 0 for t = 1 T. Define X = ∏Tt=1 Xt

a. Find E(X) and Var(X).

b. Does X follow a normal distribution or a skewed distribution?

Question 3: (Normal mixture models)

a. What is the kurtosis of a normal mixture distribution that is 95% N(0, 1) and 5% N(0, 10)?

b. Find a formula for the kurtosis of a normal mixture that is 100p% N(0, 1) and 100(1 - p)% N(0, σ2) where p and σ are parameter. Your formula should give the kurtosis as a function of p and σ.

c. Show that the kurtosis of the normal mixtures in part (b) can be made arbitrarily large by choosing p and a appropriately. Find values of p and σ so that the kurtosis is 10.000 or larger.

d. Let M > 0 be arbitrarily large. Show that for any po < 1, no matter how close to 1. there is a p > po and a a such that the normal mixture with these values of p and a has a kurtosis at least M. This shows that there is a normal mixture arbitrarily close to a normal distribution with a kurtosis above any M.

Question 4: Let X be N(0. σ2). Show that the CDF of the conditional distribution of X given that X > c is

Φ(x/σ) - Φ(c/σ)/(1-Φ(c/σ))

where x > c, and that the PDF of this distribution is

Φ(x/σ)/(σ(1-Φ(c/σ)))

where x > c. Also show that if c = 0.25 and σ = 0.3113. then at x = 0.25 this PDF equals the PDF of a Pareto distribution with parameters a = 1.1 and c = 0.25. Note: The value of σ = 0.3113 was originally found by interpolation.

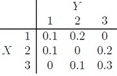

Question 5: Consider the following joint distribution of X and :

a. Find the marginal distributions of X and Y. Using these distributions. compute E(X), Var(X), SD(X), E(Y), Var(Y) and SD(Y).

b. Determine the conditional distribution of X given that Y equals 1, 2 and 3. Plot the marginal distribution of X along with the conditional distributions of X and briefly comment.

c. Determine the conditional distribution of Y given that X equals 1, 2 and 3. Plot the marginal distribution of Y along with the conditional distributions of Y and briefly comment.

d. Compute E(X|Y = 1), E(X|Y = 2), E(X|Y = 3) and compare to E(X). Compute E(Y|X = 1), E(Y|X = 2), E(Y|X = 3) and compare to E(Y).

e. Plot E(X|Y = y) versus y and E(Y|X = x) versus x and briefly comment.

f. Are X and Y independent? Fully justify your answer.

g. Compute Cov(X, Y) and Corr(X, Y).

Question 6: Let W, X, Y, Z be random variables and a, b, c, d be constants. Show that:

a. Var(aX + c)= Var(-aX - d).

b. Cov(aX, bY) = ab Cov(X, Y)

c. Cov(X, X) = Var(X).

d. Cov(aX+by, cW+dZ) = acCov(X,W)+adCov(X, Z)+bc Cov(Y, W) + bd Cov(Y, Z).

e. Suppose W = 3 + 5X and Z = 4 - 8Y.

i. Is ρY,Z = 1? Prove or disprove.

ii. Is ρW,Z = ρx,y? Prove or disprove.

Question 7: Let X and Y be two random variables.

a. If Cov(X2, Y2) = 0. then Cov(X, Y) = 0. True/False/Uncertain. Explain.

b. If X and Y are independent. then Cov(X2, Y2) > Cov(X, Y). True/False/Uncertain. Explain.

c. If X and V are independent and E(X/Y) > 1, then E(X)/E(Y) > 1. True/False/Uncertain. Explain.

d. Prove that (Cov(X, Y))2 ≤ Var(X) Var(Y) and thus -1 ≤ ρx,x ≤ 1.

Question 8: Let X and Y be independent u(-a. a) random variables. Find (a) the prob-ability that the quadratic equation t2 + tX + Y = 0 has real roots. and (b) the limit of this probability as a → ∞.