Reference no: EM13373411

Question 1:

(a) What market structure is used to benchmark allocative efficiency and why do we use it? Illustrate and explain using a diagram.

(b) Why and how do monopolistically competitive firms fail to achieve allocative efficiency? Illustrate and explain using a diagram.

Question 2:

(a) You are examining and reporting on the market performance of a very small number of firms that are known to often collude in setting output prices and quantities. Illustrate and explain using a diagram what affect this behaviour is most likely to have on the allocation of factors of production.

(b) What will happen if one of these firms cheats on the others in some way? Illustrate and explain using a diagram.

Question 3:

(a) Illustrate and explain using diagrams how a single seller within the market can maintain an inefficient allocation of resources;

(b) Are there any advantages to a single market seller and how do they compare to its perceived disadvantages.

Question 4:

(a) Assuming a constant wage rate, illustrate and explain using a diagram, how a firm's marginal costs of production are at a minimum when its marginal product is at a maximum;

(b) Illustrate and explain using a diagram how a firm's long-run average cost curve comes into existence from a multi-plant operation;

(c) Identify and describe the significance of the various portions of this diagram.

Question 5:

Illustrate and explain using diagrams, two (2) market mechanisms that are used for controlling pollution as an externality.

Question 6:

(a) Explain whether you agree or disagree with the following statement and why:

"Regardless of whether the short run or the long run is being considered, a firm should continue to operate as long as its price is greater than its average variable cost".

(b) Explain why you agree or disagree with the following statement:

"When marginal revenue equals marginal cost, total cost equals total revenue and the firm makes zero profit".

Question 7:

(a) Illustrate and explain using diagrams, the difference between long run supply in a constant cost individual firm and industry and an increasing cost firm and industry.

Question 8:

(a) Suppose the income elasticity of demand for pre-recorded music compact disks is +7 and the income elasticity of demand for a cabinet maker's work is +0.7. Compare the impact on pre-recorded music compact disks and the cabinet maker's work of an economic expansion that increases consumer incomes by 10 per cent.

(b) How might you determine whether the pre-recorded music compact discs and MP3 music players are in competition with each other?

(c) Interpret the following Income Elasticities of Demand (YED) values for the following and state if the good is normal or inferior;

YED= +0.6 and YED= -2.6

(d) Interpret the following Cross-Price Elasticities of Demand (XED) and explain the relationship between these goods.

XED= + 0.64 and XED= -2.6

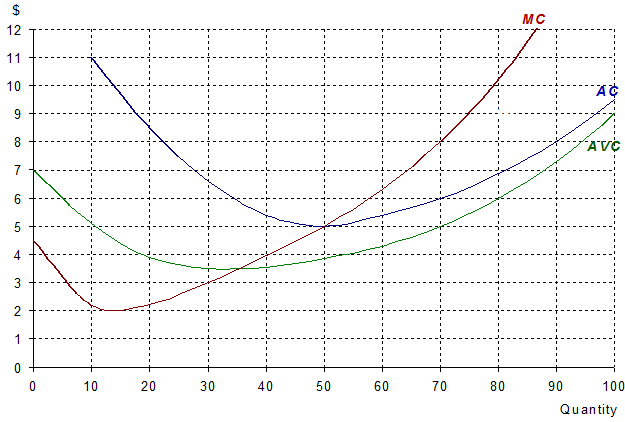

Question 9:

The following diagram shows the cost curves of a firm under perfect competition.

(a) How much will the firm produce in order to maximise profits at a price $8 per unit?

(b) What will be its average cost of production at this output?

(c) How much (supernormal) profit will it make?

(d) How much will the firm produce in order to maximise profits at a price of $5 per unit?

(e) How much (supernormal) profit will it make?

(f) How much will the firm produce in order to maximise profits at a price of $4 per unit?

(g) What will be its profit value be now?

(h) Below what price would the firm shut down in the short run?

(i) Below what price would the firm shut down in the long run?

Solve any Four Questions our of Nine