Reference no: EM132370623 , Length: word count : 1000

Assessment Type: Individual assessment-research report.

Topic: Australian Accounting Standards Analysis.

Question 1

Wayne Upton (2001, p. 71) in his discussion of the lives of intangible assets noted that the formula for Coca-Cola has grown more valuable over time, not less, and that Sir David Tweedie, former chairman of the IASB, jokes that the brand name of his favourite Scotch whisky is older than the United States of America — and, in Sir David's view, the formula for Scotch whisky has contributed more to the sum of human happiness.

Required:

Outline the accounting for brands under AASB 138/IAS 38, and discuss the difficulties for standard setters in allowing the recognition of all brands and formulas on statements of financial position.

Question 2

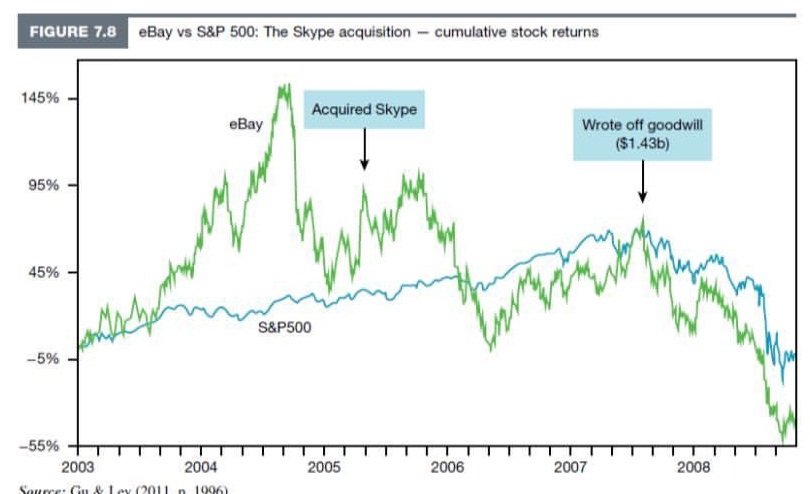

Gu and Lev (2011) argue that the root cause of many goodwill write-offs is that the shares of the buyer are overpriced at the acquisition date.

Figure 7.8 presents eBay's cumulative stock return against the S&P 500 index from 2003. In mid-September 2005, eBay acquired the internet phone company Skype for $2.6 billion. On 1 October 2007, it announced a massive goodwill write-off of $1.43 billion (55% of the acquisition price) related to the Skype acquisition.

Gu and Lev argue that the root cause of this behaviour is the incentives of managers of overvalued firms to acquire businesses, whether to exploit the overpricing for shareholders' benefit or to justify and prolong the overpricing to maintain a facade of growth. Goodwill write-offs are accordingly an important business event signalling a flawed investment strategy.

Required:

a) Explain the circumstances under which goodwill is recognised and how any subsequent write-off occurs under AASB 136.

b) Explain why a significant goodwill write-off may signal a 'flawed investment strategy'

Question 3

Tooth Ltd acquires Nail Ltd, effective 1 March 2020. At the date of acquisition, Tooth Ltd intends to close a division of Nail Ltd. As at the date of acquisition, management has developed and the board has approved the main features of the restructuring plan and, based on available information, best estimates of the costs have been made.

As at the date of acquisition, a public announcement of Tooth Ltd's intentions has been made and relevant parties have been informed of the planned closure. Within a week of the acquisition being affected, management commences the process of informing unions, lessors, institutional investors and other key shareholders of the broad characteristics of its restructuring program. A detailed plan for the restructuring is developed within 3 months and implemented soon thereafter.

Required

a) Explain the accounting for restructuring provisions with reference to AASB137.

b) Under AASB137, Should Tooth Ltd create a provision for restructuring as part of its acquisition accounting entries?

c) How would your answer change if all the circumstances are the same as those above except that Tooth Ltd decided that, instead of closing a division of Nail Ltd, it would close down one of its own facilities?