Reference no: EM131745496

Homework-

Assume we are interested in fitting an additive multiple regression model of Y on four potential covariates X1, X2, X3, X4 : , i.e. our model is Yi = β0 + β1Xi1 + β2Xi2 + β3Xi3 + β4Xi4 + εi, i = 1,...,n , where εi ~i.i.d. N (0, σ2) . The sample size is n = 17 and SST0 = 1062.21.

a) Define C′ and m for the composite hypothesis that β0 = 0, β1 + β2 = 0, and β3 = β4. That is, express as

H0: C'β = m

Ha: C'β ≠ m

b) Give the rank of C′.

c) State the reduced model for the composite hypothesis in part (a).

d) The SSE for the model Yi = β0 + β1Xi1 + β2Xi2 + β3Xi3 + β4Xi4 + εi is 37.88 and the SSE for the reduced model in part (c) is 95.11. Use the general linear test to test the hypothesis in part (a). Compute the value of the test statistic, determine the rejection region, and state your conclusion.

Note: The test statistic should be expressed in fraction form: #/# ÷ #/# as well as computing the value.

e) Compute R2 and R2adj for the model Yi = β0 + β1Xi1 + β2Xi2 + β3Xi3 + β4Xi4 + εi.

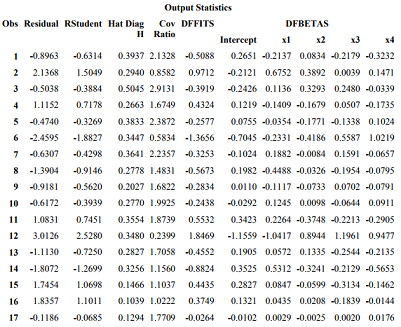

A summary of influence measures for the model Yi = β0 + β1Xi1 + β2Xi2 + β3Xi3 + β4Xi4 + εi is given below:

f) Identify which observation(s) is/are outliers, if any. Use a cutoff of 2.

g) Identify which observation(s) is/are high leverage points, if any.

h) Identify which observation(s) is/are influential on the fitted values, Yˆi , if any.

i) Identify which observation(s) is/are influential on the estimate of β0, if any.

j) Identify which observation(s) is/are influential on the estimate of β1, if any.

k) Identify which observation(s) is/are influential on the estimate of β2, if any.

l) Identify which observation(s) is/are influential on the estimate of β3, if any.

m) Identify which observation(s) is/are influential on the estimate of β4, if any.

Attachment:- Assignment.rar