Reference no: EM131805518

A call option on common stock is being evaluated. If the stock goes down, the option will expire worthless. If the stock goes up, the payoff depends on just how high the stock goes.

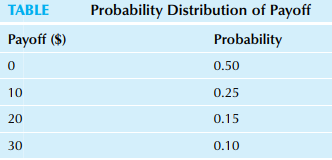

For simplicity, the payoffs are modeled as a discrete distribution with the probability distribution in Table .

Even though options markets, in fact, behave more like a continuous random variable, this discrete approximation will give useful approximate results.

Answer the following questions based on the discrete probability distribution given.

a.Find the mean, or expected value, of the option payoff.

b.Describe briefly what this expected value represents.

c.Find the standard deviation of the option payoff.

d.Describe briefly what this standard deviation represents.

e.Find the probability that the option will pay at least $20.

f.Find the probability that the option will pay less than $30.