Uses of Break Even Analysis

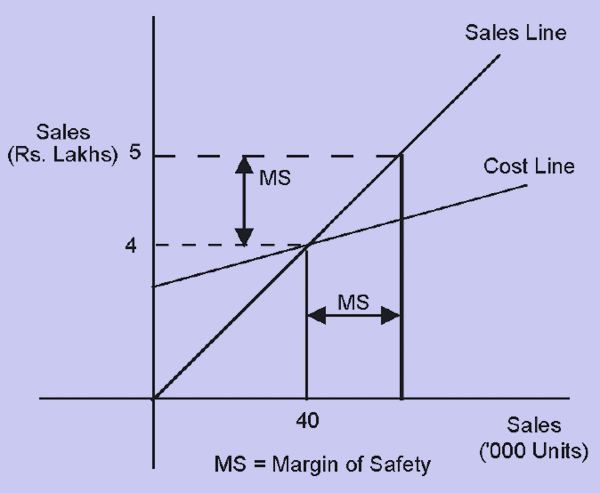

For example, in the above case sales should be at least 40,000 units or Rs.4 lakh before the firm starts earning a profit.

In the example above, break even sales are at Rs.4 lakh. Actual sales are expected to be Rs.5 lakh. Then if actual sales are lower by more than 10,000 units, Rs.1 lakh or 20%, the firm will incur losses.

The 10,000 units or Rs.1 lakh or 20% is called the Margin of Safety. It is the difference between actual sales and Break Even sales.

Consider the three cases illustrated below:

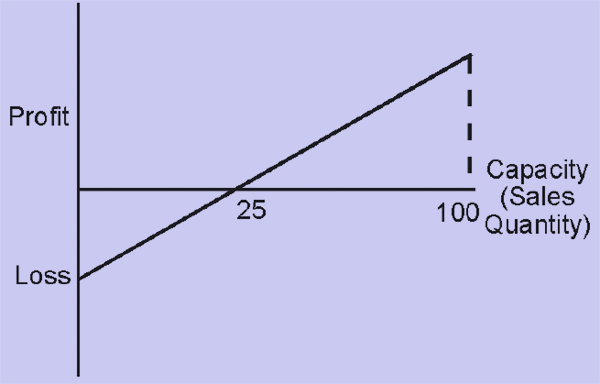

Case I

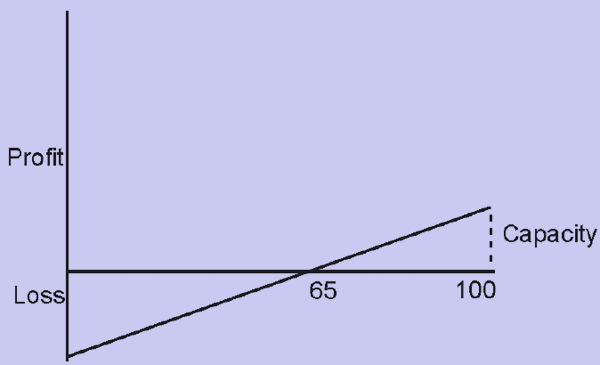

Case II

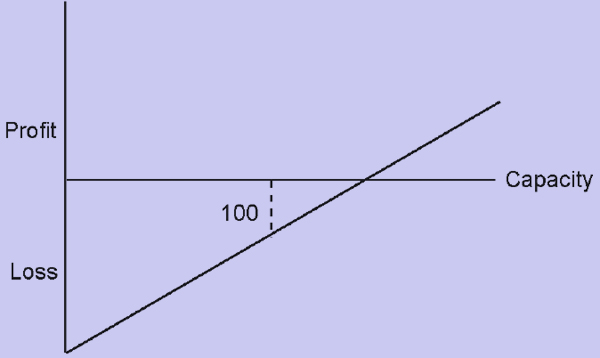

Case III

In all the cases, the firm has a capacity of 100%. This means that the company does not have the necessary infrastructure to produce more than 100 units in a year [capacity is usually specified as maximum possible production per year].

-

In Case I, once the sales quantity crosses 25 units or 25% of capacity, the firm begins to earn a profit. This is relatively a safe situation because the firm can start earning profit at a relatively low level of activity.

-

In Case II, the firm begins to earn a profit once the sales quantity crosses 65 units or 65% of capacity. This is a riskier situation than Case I because the firm has to achieve a much higher level of activity before it can start earning profits.

-

Case III is a disaster because the firm cannot earn a profit even when sales quantity equals the capacity of 100 which is the maximum possible production.

Email based Accounting assignment help - homework help at Expertsmind

Are you searching Accounting expert for help with Uses of Break Even Analysis questions? Uses of Break Even Analysis topic is not easier to learn without external help? We at www.expertsmind.com offer finest service of Accounting assignment help and Accounting homework help. Live tutors are available for 24x7 hours helping students in their Uses of Break Even Analysis related problems. We provide step by step Uses of Break Even Analysis question's answers with 100% plagiarism free content. We prepare quality content and notes for Uses of Break Even Analysis topic under Accounting theory and study material. These are avail for subscribed users and they can get advantages anytime.

Why Expertsmind for assignment help

- Higher degree holder and experienced experts network

- Punctuality and responsibility of work

- Quality solution with 100% plagiarism free answers

- Time on Delivery

- Privacy of information and details

- Excellence in solving Accounting questions in excels and word format.

- Best tutoring assistance 24x7 hours